#4 Allterco JSCo (Now Shelly Group)

Take control of your energy costs

Update: In July 2023 the company has changed it’s name from Allterco to Shelly Group as their main product line is Shelly. So whenever you will read Allterco in this write-up it should now be Shelly.

Welcome,

in this issue of Under-Followed-Stocks I will present you Allterco JSCo ($A4L).

Investment Summary:

Up to 30 % less energy consumption through Allterco’s home automation solutions (“Shelly”)

Acceleration of profitable growth, supported by strong tailwinds: In the first 9 months of 2022, they achieved revenue growth of 55% accelerating from 35% after 6 months and an industry-leading EBIT-Margin of 23.8%

The company expects to grow by over 40% per year until 2025 supported by international expansion, professionalization of sales & overall secular growth in the IoT market

LTM EV/EBIT multiple of 17.5x

Founder-led with 65% insider ownership and a clean balance sheet

If you aren’t a subscriber yet and enjoy my content, feel free to subscribe so that you won’t miss any new content.

Disclaimer: The following write-up is no investment advice. The author may own, buy and sell securities mentioned in this post. Please always do your own due dilligence!

Let’s go!

1. Introduction

Allterco JSCo is a Bulgarian company that develops smart home products. They offer affordable and high-quality home automation products under their "Shelly" brand through B2B partners, own websites (D2C) and marketplaces like Amazon, mainly in Europe.

Allterco was founded in 2003 as a telecommunications company. 10 years later the IoT unit of the company was established with the development of the first home automation system, which laid the foundation of the well-known brand “Shelly”. In 2015 the corporation was completely restructured with the affiliate IoT-focused company Allterco Robotics being established. The successful development and realization of IoT products not only in Bulgaria but also in the international markets led to the strategic decision to sell the European telco business in 2019 and the Asian telco business in 2021 to put the focus entirely on the areas of IoT.

The company is listed on the Bulgarian Stock Exchange (BSE:A4L) since 2016 and since 2021 also in Frankfurt (FRA:A4L). Reporting currency is lev (BGN) and the current market cap is 359 million BGN (USD 191 million) with a free float of only 35 %.

2. The Market

With its “Shelly” products, Allterco is mainly active in the following smart home segments:

Control & Connectivity

Security

Comfort & Lighting

Energy Management

According to Statista, the overall smart home market in Europe is expected to grow with a CAGR of 14.6 % from 2022-2026 reaching a market volume of USD 50.3 billion. The CAGR’s (22-26) in Alltercos core markets are between 14.2 % (Energy Management) and 16.5 % (Control & Connectivity).

Between 2019 and 2021 the overall smart home market grew with a CAGR of 25 %. Since Allterco started focusing on IoT devices in 2019, they were able to outperform the market with a product revenue CAGR of 72% from 2016 - 2021.

Google, Apple, and Amazon dominate some segments of the smart home market, such as smart speakers. Allterco, on the other hand, has positioned itself more in a niche and fragmented market. The Products section of this write-up discusses how Allterco differentiates its products from its competitors.

3. Products

Allterco has 2 product lines. In the “Myki” line, Allterco is distributing smartwatches, specifically for children as well as tracking devices for cars, pets, baggage, or health care data.

In their “Shelly” line, Allterco is offering their innovative IoT devices which allow remote control of electric appliances through mobile phones, PC or home automation systems. Shelly’s portfolio lays the foundation for its relays, allowing for remote control of lights, electrical appliances, sensors, bi-directional motors, as well as monitoring of energy consumption. Additionally, Shelly’s portfolio includes intelligent wall plugs, air purifiers, temperature & humidity sensors, and smart dimmable and RGBW bulbs.

Shelly devices are used by more than 2 million households, and they have sold more than 7 million units since they were launched. As a result of accelerated sales, they were able to sell 1 million devices in Q3 2022 alone and during the recent Black Friday event they even managed to sell half a million devices alone. Shelly devices are installed every 7.7 seconds, making it one of the fastest-growing smart home brands worldwide in their segment.

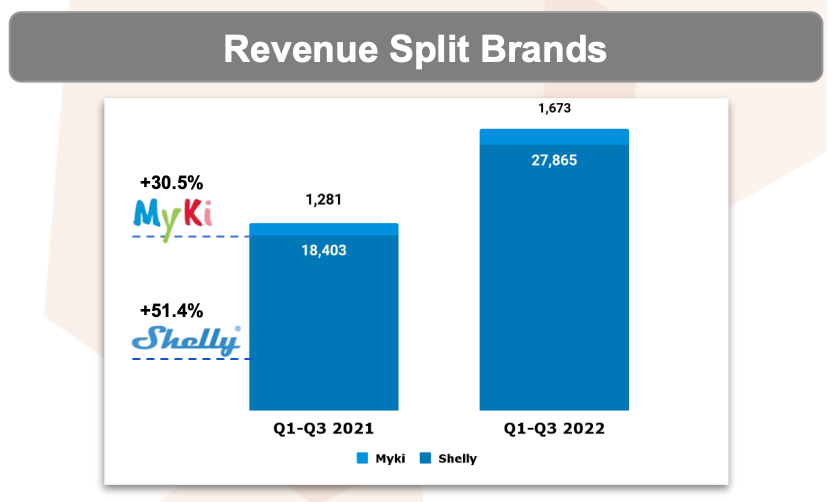

Both segments are growing strong. Myki with 30.5 % in the 9 months of ‘22 and Shelly with 51.4 %. But as the MyKi share of total revenue is only 5.6 % I will focus on the opportunities and risks in the Shelly segment in this write-up.

What differentiates the Shelly products from their competitors?

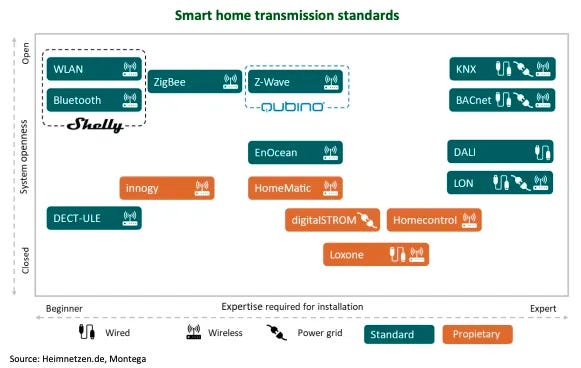

Open-system: Shelly devices are compatible with all open and common smart home platforms. Shelly also published a secure cloud API access. This allows 3rd part programs to control the shelly devices through the shelly cloud. Shelly’s product philosophy is to guarantee maximum openness to systems.

Transmission standard: Shelly is focusing on Bluetooth and WLAN as transmission standards. Compared to other standards like ZigBee or Z-Wave you don’t need to buy additional expensive bridges/gateways to connect your smart home devices to your home network which makes it also easier to install. Shelly will also support the “Matter” standard as soon as it’s available. With the acquisition of Qubino, which is likely to be finalized this December, Allterco will also offer the Z-Wave technology that is often used in US-Security Businesses.

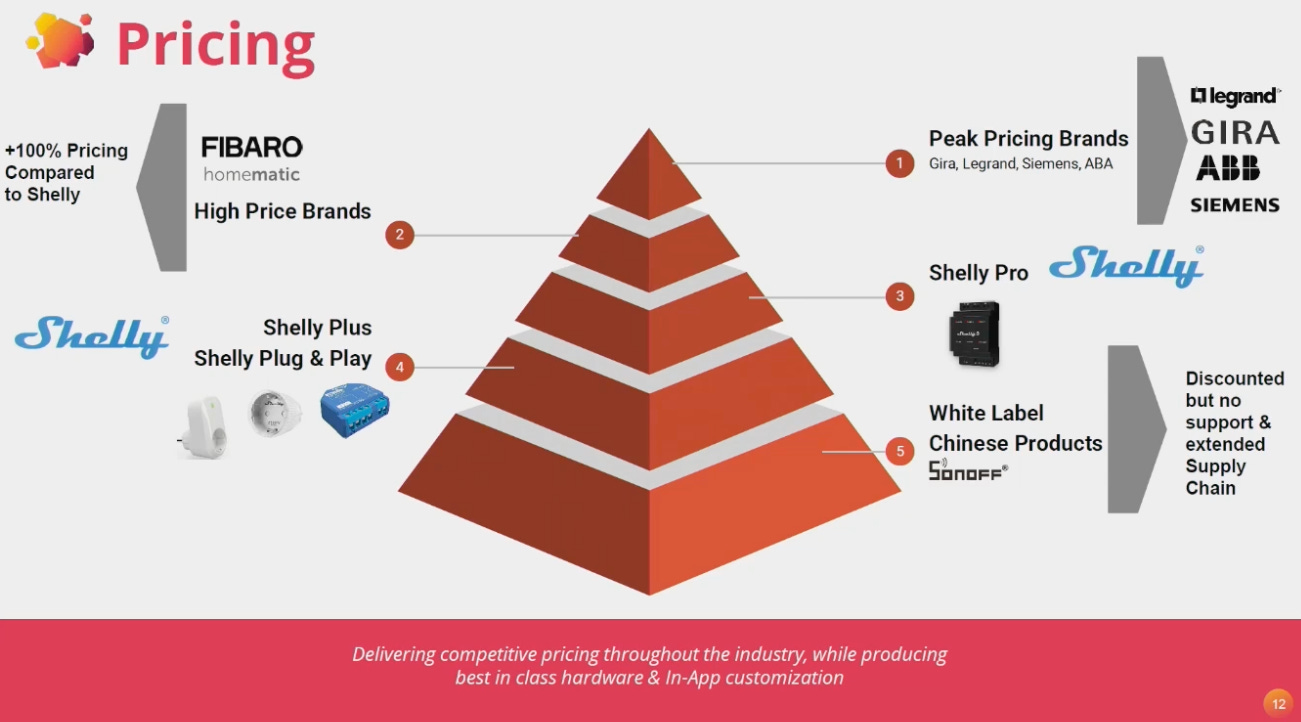

Positioning as an affordable European brand: Shelly products are positioned at the lower end of the price range, while most of the other European / Western competitors are positioned in the high(er) price range. The lean and attractive cost structure in Bulgaria allows Allterco to still achieve solid margins, despite the lower price range. Especially retrofitting older buildings with affordable Shelly products generates a high value for the customers as the costs for the home automation are amortized very fast due to lower energy consumption enabled by the automation.

Compared to Asian competitors, which are partially lower in price, Shelly can convince customers with their perception as a European quality brand. Smart Home appliances are recording a lot of sensible data from their users. Customers may be concerned about the security of non-European providers. Alltercos’s cloud is based in Germany and fulfills the highest security standards. In addition, all Shelly products can also be used without cloud storage.

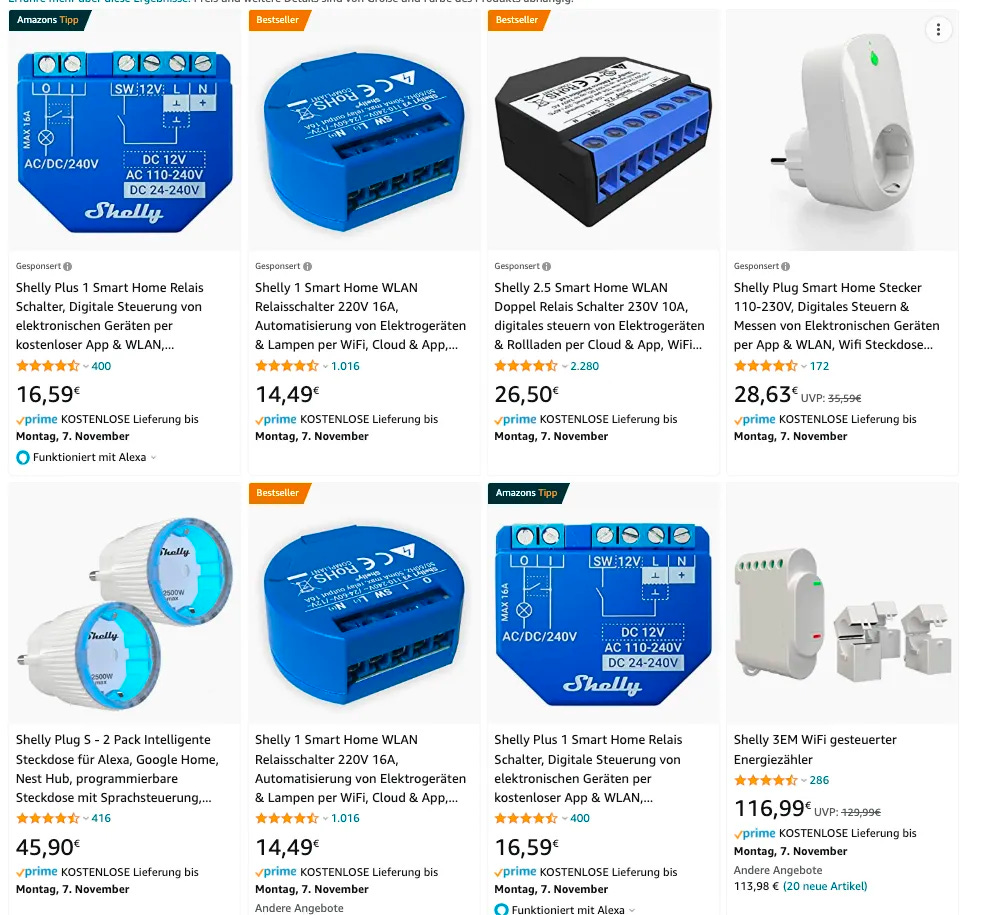

Good reviews as an asset: Many B2C customers are searching for their first Smart Home products on marketplaces like Amazon. Thus, good reviews on these platforms are an important asset. Most of the Shelly products are rated with 4.5 stars and more. The Shelly Plus 1 is also presented as Amazon’s tip, while the Shelly 1 and 2.5 are presented as Bestsellers. These Smart Home relais are often the starting point for people who wants to retrofit their homes to smart homes. Once installed into the switches of their house, it is more likely that these customers are also looking for others products of the Shelly line like sensors as they’re already familiar with the installation process and the Shelly Cloud platform.

Customer engagement: Shelly products have a high level of customer engagement. Looking into Shelly support groups on Facebook or several Youtube Videos, there are many customers that are exchanging ideas on how to integrate their “Shelly’s” the best way into their smart homes and new ideas about useful automation tasks with Shelly. Allterco is also directly communicating with their customers in these groups. Customers give feedback on new products or updates, and management actively asks for new products or improvements their customers want. The official support groups on Facebook and other channels have over 100k active members (there are also more unofficial country-specific groups). According to Allterco, they have over 1 million reaches on Facebook & Instagram.

4. Growth Driver

The IoT market and especially the smart home automation market in Europe (to save energy) is expected to grow significantly in the next years. But besides these overall secular growth trends, there are also some more specific growth trends for Allterco:

Professionalization of sales & marketing: Sales activities at Allterco have been low until 2022. Their growth was mainly due to word of mouth. Looking at the sales development it is impressive how efficient this small sales team has been in the past. Since November 2021, Wolfgang Kirsch is responsible for the international sales activities of Allterco as a Co-Ceo. Previously, Kirsch was leading the international expansion of the MediaMarktSaturn Retail Group (Europe’s leading consumer electronics retailer). Expanding B2B sales in new regions will be a focus area. Kirsch decided to establish dedicated sales teams for these regions. The ramp-up started with the DACH region in Q2 2022. The first effects of this ramp-up are expected to materialize in Q4 ‘22 / Q1 ‘23.

Furthermore, Allterco is improving its BC2 channels since their online presence is outdated both technically and graphically. New shops with better UX, local languages, better SEO/SEA and better logistic processes are already planned and the dedicated german shop already went online right after Black Friday. The new online shop in the US is already online a bit longer, selling 20 % more than the old one without further marketing or SEO investments. The new shops with local languages in the other european countries are also expected to go online soon.

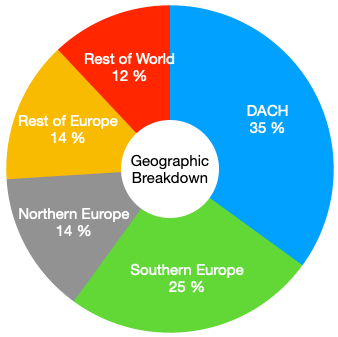

International Expansion: Besides the DACH region (Germany, Austria, Swiss), Allterco is also planning to increase their sales activities in other European countries like France, UK, Spain, Portugal, Italy, the Nordics and Benelux. Germany is the biggest market for Allterco at the moment, but France & UK offer similar opportunities regarding market size. Allterco already hired a salesperson for France. Additionally, the first investments have already been made in the Americas and also Asia. There is still a lot of room for growth in the international expansion.

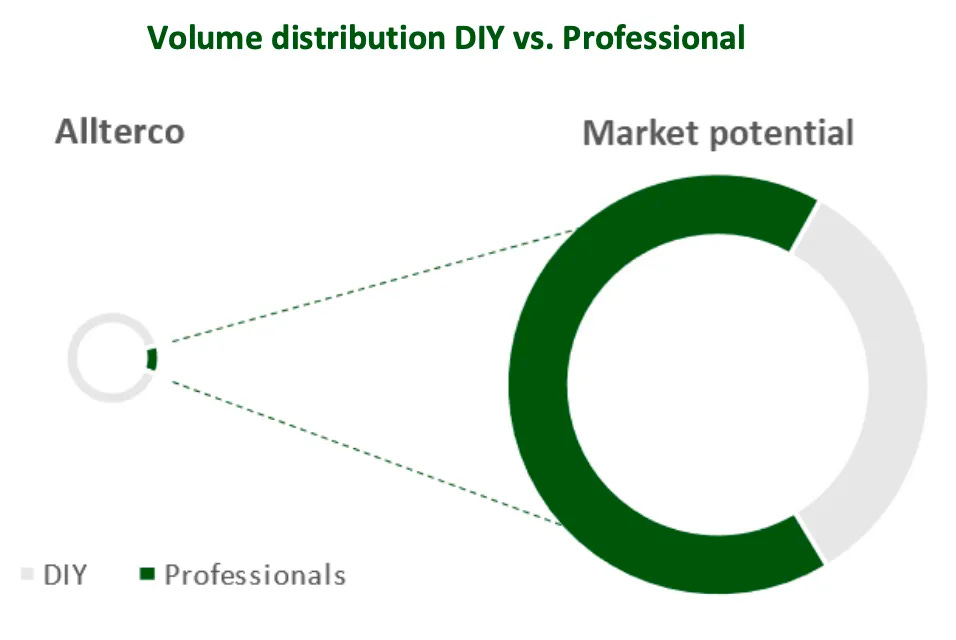

Expansion of product portfolio & recurring revenues: Currently, most of the Shelly products are relays and measuring devices. The company wants to gradually expand its product portfolio over the next years, especially in professional applications as well as plug-and-play devices. Allterco is planning a Pro-Series of their products with VDE & UL certification that is targeting professional users. This customer group is currently underrepresented, but it offers huge potential.

The Shelly devices are collecting a vast amount of data, especially regarding energy consumption or heating. The user already gets a great overview & visualization of the energy consumption in his household. In order to save more energy, Allterco can analyze this data and offer advice to customers. This premium feature, among others, will be implemented into the completely new App that Allterco is currently working on. To get these additional features, the customers will have to pay a monthly fee. Large business customers are using the Shelly API to implement the data into their own interfaces. For some use cases, they need a big amount of data at a high speed. One customer for example asked to get the consumption data every 100 milliseconds instead of normally every 15 seconds and that they would pay for this additional service. So Allterco has options to generate recurring revenue in the DIY and also in the professional market to enhance their growth and margins.

5. Management & Shareholders

Dimitar Dimitrov is the founder of the IoT business of Allterco and with a stake of nearly 33 %, he is also one of the largest shareholders. Today he serves as the Group CEO and Head of R&D division. Previously to Allterco, Mr. Dimitrov has already established other IT companies. He started his first company shortly before graduating from high school, which specialized in software development for 8 and 16-bit computers. He is also the founder of the newspapers PC Review, Computers and Peripherals, and GSM Review.

Svetlin Todorov has Co-established Allterco JSCo and also owns nearly 33 % of the company. He has more than 20 years of experience in the sector of telecommunications, media and technology. He is currently responsible for US operations and Business Relations.

As already mentioned, Wolfgang Kirsch joined Allterco in 2021 as Co-Ceo and Chief of Allterco Europe. With over 25 years of experience in consumer electronics retailers in Europe, he is made for the job to develop and expand Allterco’s European business through sales and marketing.

6. Financials

As you can see below, Allterco was able to grow its revenues in the first 9 months of 2022 by 55%. Due to planned higher investments in sales and R&D, the EBIT grew “only” by 22.9%, but Allterco was still able to achieve an industry-leading EBIT-Margin of 23.8%.

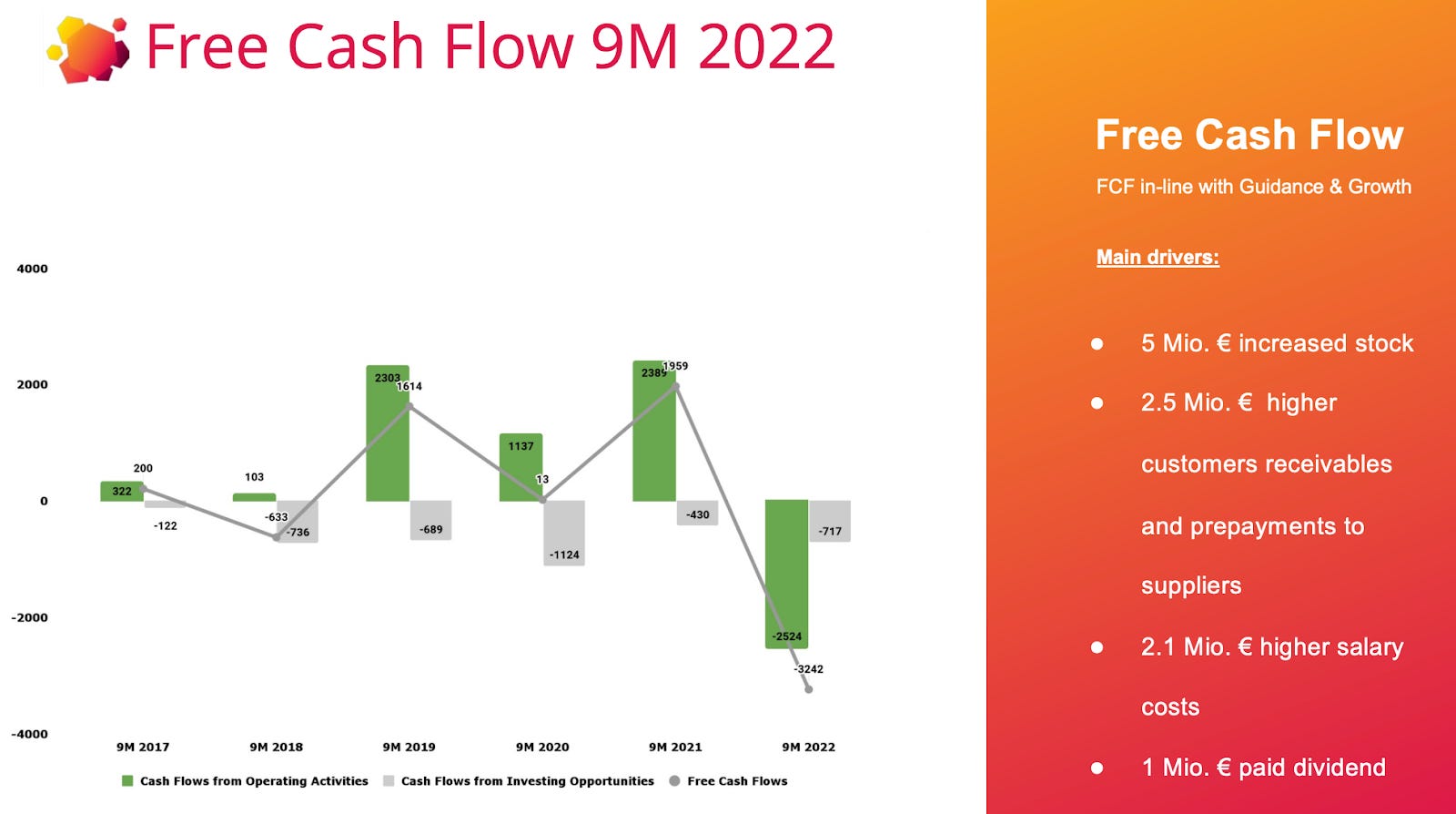

Allterco has a clean balance sheet with an equity ratio of over 90 % and net cash. In line with expectations, the operating Cashflow decreased to EUR -2.5 million and the free cashflow to EUR -3.2 million. The management decided to increase their stock level by EUR 5 million to manage the higher sales and to be prepared for possible supply chain issues as their products are made in China. And looking currently at China and how their Zero-Covid politics work, this is probably a good decision. A further negative driver has been EUR 2.5 million higher customer receivables and prepayments to suppliers, EUR 2.1 million higher salary costs and EUR 1 million paid dividend. The B2B market is growing faster than the D2C market, so Allterco has to offer different payment terms to professional wholesalers, impacting free cashflow negatively. Allterco's strong cash position allows it to continue growing without requiring additional capital.

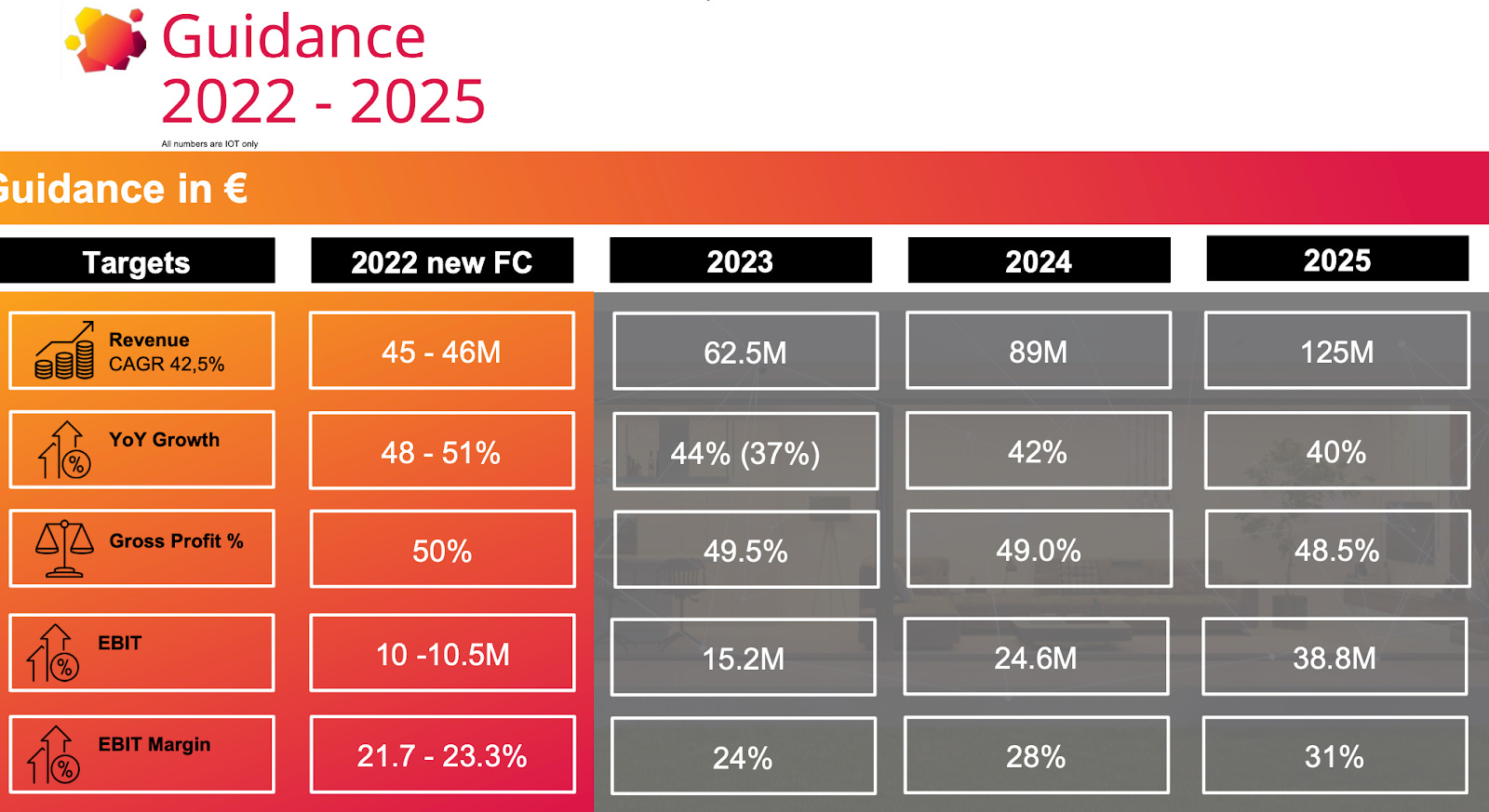

Based on a solid order backlog and a strong start in the final quarter, Allterco had to raise its full-year guidance for 2022. The company is now expecting revenues between EUR 45-46 million (up from EUR 43.5) at an EBIT-Margin between 21.7 % - 23.3 % (up from 22 %).

2022 is a year with planned higher investments. In the coming years, the management is expecting to increase the margins again to a level they already had in 2021 (31 %). The high investments in sales should also increase the revenues in the future. It is expected that revenues will increase from EUR 45 million in 2022 to EUR 125 million in 2025, resulting in a CAGR of 42.5%. As they already overachieved their targets in 2022, management is even considering upgrading their 2025 guidance.

7. Valuation

Allterco currently has an Enterprise Value of USD 169 million and is valued at an EV/EBIT of 16.8 and P/E of 23 while it is expected to grow its top line by 37% with a higher EBIT-Margin in 2023.

Below you can see the valuation of some publicly listed IoT competitors (Peer Group). Not all of them are pure-play Smart Home companies like Allterco and that’s why the expected growth rates and margins differ.

I think the most similar company is Plejd regarding the products they offer (mostly smart relays) and also the size (EV of USD 222 million). Plejd has an installed base of over 2 million devices and generated USD 41 million in sales in the last twelve months. Plejd is expected to grow by 28% in 2023 and is currently valued with an EV/EBIT of 30.5.

So, Allterco has a 3.5x higher installed base, generated 85% higher sales in the last twelve months, has a higher EBIT-Margin and is expected to grow faster in 2023. Still, Allterco's valuation is only about half that of Plejd when you look at EV/EBIT.

What’s the reason for that? I think some investors are afraid of investing in a Bulgarian company and prefer a Swedish company like Plejd. Furthermore, Allterco as a listed company is still unknown. Their Shelly brand is well known in the smart home segment in Europe, but most customers don't know that the listed company Allterco is behind it. The management started in 2022 to visit some investor conferences, especially in Germany which is their biggest market and where they also have a second listing to bring more attention to their stock. The Management recently mentioned, that switching their official company headquarter is a possibility in the future. Additionally, Deloitte replaced their well-known Bulgarian auditor, which should also increase investors trust in the company and their financials.

Another interesting competitor is Somfy. The French company offers smart home products to control for example your shutters, lights or gates. On 15th November 2022 the Despature family announced an offer to take Somfy private. The family group already owns 73.9 % of Somfy’s share capital and offered 143 € per share, representing a premium of 38.5 %, with the aim of a squeeze-out. This offer implies a valuation multiple of 15x EBIT. This multiple is just slightly below the multiple of Allterco currently, but analysts expect almost no growth for Somfy in 2023 compared to Allterco's anticipated strong growth and higher margins.

8. Risks

China manufacturing / Supply Chain Issues: Allterco’s products are manufactured in China (like most products of their competitors). Any issues in China, either political nature or Covid-related, could have a significant impact on Allterco’s ability to meet the demand. In the past, Allterco was able to react fast. During the chip shortages for example, the products were quickly modified by the engineers so that they could use other chips that were still available. In addition, the management is trying to mitigate the risks by building up higher inventory.

Competition: As already outlined, the IoT market is expected to grow fast in the future and looking at the margins that Allterco is able to achieve, other companies with deeper pockets will be attracted. Companies that are able to enter the market with dumping prices to gain market share. This could have an impact on Allterco’s pricing advantage and margins.

Growth of IoT market: The growth forecasts of the IoT market are eventually too optimistic. Remember when Amazon, Apple, Google & Co. introduced their smart speakers? Many thought we will be able to speak with Alexa & Co. like we do it with real persons or give them tasks that will make our everyday life easier. Well, the reality now is disappointing. Most people only use Alexa as a timer or maybe to switch some lights on & off. Amazon is now even thinking about cutting its costs for Alexa. Expectations and reality often differ. The smart speaker from the big tech companies are seen as enablers for Allterco’s products. If these smart speakers are not used as heavily as expected, this could also be the case for other IoT devices.

Data security & defective products: Allterco is collecting a huge amount of private data from their customers. If they’re not able to keep this data secure, this would have a huge impact on customers' trust to share their data in Allterco’s cloud (which is not mandatory).

Shelly’s relays are directly connected to the house's electricity. Defective products can cause a short circuit or similar, which could result in considerable damage. If this is attributable to Allterco, this could represent a risk for the company.

9. Summary

We have long been promised a smart home that makes our everyday lives easier. But no major benefits for consumers have yet emerged. Until now? With energy costs rising sharply, the incentive to save energy is now much greater. The easiest way to achieve this is to use energy only when it is actually needed. And that can be automated with smart devices. With Allterco's cost-effective Shelly products, added value is quickly created for the customer. As an unknown Bulgarian company, Allterco is currently undervalued compared to its international peers as long as they’re able to continue to outperform the market and gain further market share. The management has high ambitions. They have to prove that they’re able to deliver as they promised. For 2022, they already delivered.

Great writeup! Seems like a really interesting company. I think the consumer aspect is the key here. It’s great to see that their ratings are high and their customer engagement is strong. My one question/concern would be where does this fall into a consumer’s hierarchy of need? For example: if there is a downturn in the European economy how high on consumer’s list of priorities would their products be?